When it comes to managing personal finances, few names carry as much weight as Dave Ramsey. Known for his no-nonsense advice and practical strategies, Ramsey has become a household name in financial literacy. Among his many teachings, his stance on debt consolidation loans stands out. For those burdened by mounting debts, Dave Ramsey's approach offers not just solutions but also a pathway to financial freedom. By focusing on the psychology of debt, Ramsey emphasizes that debt consolidation loans aren't always the silver bullet they’re marketed to be. Instead, he advocates for a disciplined and structured approach to eliminating debt entirely. His methods, though unconventional to some, have helped countless individuals regain control of their financial lives.

Understanding Dave Ramsey’s perspective on debt consolidation loans requires delving into his broader philosophy on debt. Ramsey believes that financial health isn’t just about numbers; it’s about habits, mindset, and long-term commitment. His teachings often revolve around the idea that true financial freedom comes from eliminating debt entirely, rather than simply reorganizing it. While debt consolidation loans might seem like a quick fix, Ramsey warns against the dangers of relying on them without addressing the root causes of financial struggles. His advice is straightforward yet powerful: tackle debt head-on, one step at a time.

In this article, we’ll explore Dave Ramsey’s views on debt consolidation loans in depth. From understanding his background and philosophy to dissecting his strategies, you’ll gain a comprehensive understanding of why his approach is so effective. Whether you’re considering a debt consolidation loan or simply looking for ways to improve your financial health, this article will provide actionable insights and practical advice. Let’s dive in and uncover the transformative power of Dave Ramsey’s teachings on debt management.

Read also:The Ultimate Guide To Body Rubs In Richmond Va Enhance Your Wellness Journey

Table of Contents

- Who Is Dave Ramsey? – A Brief Biography

- What Are Debt Consolidation Loans?

- Why Does Dave Ramsey Disapprove of Debt Consolidation Loans?

- How Can You Avoid Falling Into the Debt Consolidation Trap?

- Is Debt Consolidation Ever a Good Idea?

- Why Does Dave Ramsey Promote the Debt Snowball Method?

- What Are the Alternatives to Debt Consolidation Loans?

- How Can You Stay Motivated While Paying Off Debt?

- Frequently Asked Questions

- Conclusion: Embrace Financial Freedom the Ramsey Way

Who Is Dave Ramsey? – A Brief Biography

Dave Ramsey is more than just a financial expert; he’s a beacon of hope for millions struggling with debt. Born on November 3, 1960, in Antioch, Tennessee, Ramsey has built a career around helping people achieve financial peace. Before becoming a household name, Ramsey faced his own financial challenges, including bankruptcy at the age of 26. This personal experience fueled his passion for teaching others how to avoid the same pitfalls.

Ramsey’s journey into financial education began in the early 1990s when he started hosting a radio show called "The Dave Ramsey Show." Over the years, this show evolved into a national phenomenon, reaching millions of listeners daily. Through his best-selling books, podcasts, and live events, Ramsey has empowered countless individuals to take control of their finances. His flagship program, Financial Peace University, has been instrumental in helping people eliminate billions of dollars in debt.

Below is a summary of Dave Ramsey’s personal details:

| Full Name | Dave Ramsey |

|---|---|

| Date of Birth | November 3, 1960 |

| Place of Birth | Antioch, Tennessee |

| Profession | Financial Educator, Author, Radio Host |

| Notable Works | Financial Peace University, The Total Money Makeover |

What Are Debt Consolidation Loans?

Debt consolidation loans are financial tools designed to simplify the debt repayment process. Essentially, these loans allow borrowers to combine multiple debts into a single loan with a lower interest rate and more manageable monthly payments. While this approach can seem appealing, it often comes with hidden risks and drawbacks. For instance, extending the repayment period may result in paying more interest over time, negating the initial savings.

Debt consolidation loans are commonly used to address credit card debt, medical bills, and other forms of unsecured debt. Financial institutions market these loans as a way to reduce stress and streamline payments. However, as Dave Ramsey points out, they don’t address the underlying causes of debt. Without a change in spending habits and financial behavior, individuals may find themselves back in the same situation—or worse—after consolidating their debts.

How Do Debt Consolidation Loans Work?

When you opt for a debt consolidation loan, the lender pays off your existing debts on your behalf. You then repay the loan over an agreed-upon term, typically with a fixed interest rate. While this can simplify your financial life by reducing the number of payments you make each month, it’s crucial to evaluate whether the long-term costs outweigh the benefits.

Read also:Delicious And Nutritious Meals For Picky 2yearolds A Parentrsquos Ultimate Guide

Key Considerations Before Taking Out a Debt Consolidation Loan

- Interest Rates: Ensure the new loan offers a significantly lower rate than your current debts.

- Repayment Terms: Longer terms may lower monthly payments but increase overall interest costs.

- Hidden Fees: Watch out for origination fees, balance transfer fees, and prepayment penalties.

Why Does Dave Ramsey Disapprove of Debt Consolidation Loans?

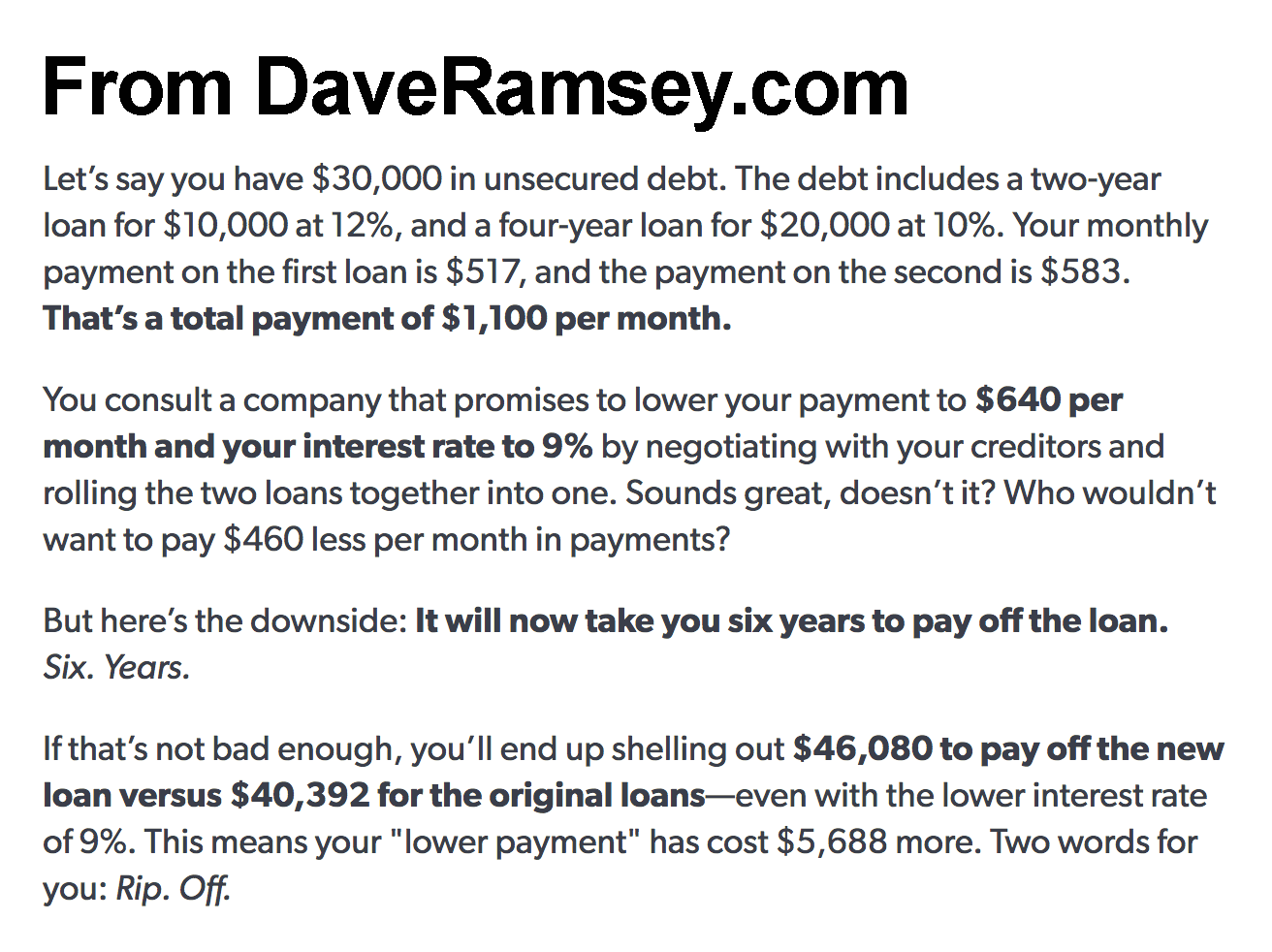

One of the central tenets of Dave Ramsey’s philosophy is that debt is not a tool for financial growth but rather a hindrance to achieving true freedom. When it comes to debt consolidation loans, Ramsey argues that they perpetuate the cycle of debt rather than breaking it. By rolling multiple debts into a single loan, individuals may feel a false sense of relief, which can delay the necessary behavioral changes required for lasting financial health.

Ramsey believes that debt consolidation loans often fail to address the root causes of financial struggles. Instead of encouraging discipline and accountability, these loans can enable continued reliance on borrowing. His approach emphasizes the importance of facing debt head-on, without relying on external solutions that don’t tackle the problem at its core.

What Are the Risks of Debt Consolidation?

While debt consolidation loans may seem like a straightforward solution, they carry several risks:

- Extended Repayment Periods: Stretching out payments can lead to higher interest costs over time.

- Increased Borrowing Temptation: Consolidating debt can free up credit lines, tempting individuals to accrue new debts.

- Failure to Address Spending Habits: Without changing financial behaviors, the cycle of debt continues.

How Can You Avoid Falling Into the Debt Consolidation Trap?

Preventing reliance on debt consolidation loans starts with understanding the alternatives and adopting healthier financial habits. Dave Ramsey advocates for a proactive approach to debt management, emphasizing education and discipline. By focusing on the root causes of debt, individuals can create a sustainable plan for financial freedom.

To avoid falling into the debt consolidation trap, Ramsey suggests:

- Creating a Detailed Budget: Track income and expenses to identify areas for improvement.

- Building an Emergency Fund: Set aside money for unexpected expenses to avoid relying on credit.

- Eliminating Unnecessary Expenses: Cut back on non-essential spending to free up more resources for debt repayment.

Is There a Better Way to Manage Debt?

Absolute financial freedom begins with a mindset shift. Instead of seeking quick fixes, focus on building long-term solutions. Ramsey’s teachings encourage individuals to take ownership of their financial futures, one step at a time.

Is Debt Consolidation Ever a Good Idea?

While Dave Ramsey strongly discourages the use of debt consolidation loans, there may be rare circumstances where they could be beneficial. For instance, if someone is drowning in high-interest credit card debt and has no other viable options, a consolidation loan with a significantly lower interest rate might provide temporary relief. However, even in such cases, Ramsey stresses the importance of combining this strategy with a comprehensive plan for eliminating debt entirely.

Ultimately, the decision to pursue a debt consolidation loan should be made with caution and careful consideration of all available alternatives. Ramsey’s advice remains consistent: address the root causes of debt and prioritize long-term solutions over short-term fixes.

When Might Debt Consolidation Make Sense?

In limited scenarios, debt consolidation could be a reasonable option:

- When interest rates on existing debts are prohibitively high.

- If the borrower has a clear plan to avoid future debt accumulation.

- In cases where consolidating debts simplifies repayment without extending the term excessively.

Why Does Dave Ramsey Promote the Debt Snowball Method?

At the heart of Dave Ramsey’s debt elimination strategy lies the debt snowball method. This approach involves listing all debts from smallest to largest and focusing on paying off the smallest ones first while making minimum payments on the rest. Once the smallest debt is eliminated, the money allocated to it is rolled into the next smallest debt, creating a "snowball" effect that accelerates progress.

Ramsey champions the debt snowball method because it provides psychological motivation. By seeing quick wins, individuals stay encouraged and committed to their financial goals. This method emphasizes momentum and discipline, key components of Ramsey’s overall philosophy.

How Effective Is the Debt Snowball Method?

Research and real-world success stories demonstrate the effectiveness of the debt snowball method. Studies have shown that individuals who use this approach are more likely to stick with their debt repayment plans compared to those who prioritize larger debts first. Ramsey’s emphasis on behavior change makes the debt snowball method not just a financial strategy but a psychological one as well.

What Are the Alternatives to Debt Consolidation Loans?

For those seeking alternatives to debt consolidation loans, Ramsey offers several practical solutions. These include negotiating with creditors for lower interest rates, utilizing the debt snowball method, and exploring community resources such as credit counseling services. By leveraging these options, individuals can address their debts without incurring additional financial burdens.

Additionally, Ramsey encourages the use of cash-based transactions to break the cycle of reliance on credit. By shifting to a cash-only system, individuals can avoid accruing new debts while focusing on repaying existing ones.

Can Credit Counseling Help?

Credit counseling services can provide valuable support for those overwhelmed by debt. These organizations often offer debt management plans that negotiate reduced interest rates and fees with creditors. However, Ramsey advises caution when choosing a credit counseling service, ensuring it’s reputable and aligned with your financial goals.

How Can You Stay Motivated While Paying Off Debt?

Paying off debt is a marathon, not a sprint. Staying motivated throughout the journey requires a combination of goal-setting, accountability, and celebration of milestones. Ramsey suggests setting specific, measurable financial goals and sharing them with a trusted accountability partner. Regularly reviewing progress and rewarding achievements can keep motivation high.

Visualization techniques, such as creating a debt payoff thermometer or tracking progress on a spreadsheet, can also boost motivation. Ramsey’s teachings emphasize the importance of celebrating small victories along the way, reinforcing positive behaviors and maintaining momentum.

What Are Some Practical Ways to Stay Inspired?

Here are a few strategies to stay inspired during your debt repayment journey:

- Join a community of like-minded individuals for support and encouragement.

- Read success stories of others who have achieved financial freedom.

- Revisit your "why"—the reasons you started this journey—to reignite your passion.

Frequently Asked Questions

Can Debt Consolidation Loans Work Without Changing Spending Habits?

No, debt consolidation loans alone are unlikely to resolve financial issues unless accompanied by a change in spending habits. Without addressing the root causes of debt, individuals may find themselves back in the same situation shortly after consolidating their debts.

Is the Debt Snowball Method Better Than the Debt Avalanche Method?

Both methods have their merits, but Ramsey prefers the debt snowball method due to its psychological benefits. While the debt avalanche method prioritizes high-interest debts first, the snowball method focuses on quick wins to maintain motivation.

How Long Does It Take to Pay Off Debt Using Dave Ramsey’s Methods?

The time required to pay off debt varies based on the amount owed, income level, and commitment to the process. Ramsey’s methods emphasize consistency and discipline, with many individuals achieving significant progress within months or years.

Conclusion: Embrace Financial Freedom the Ramsey Way

Dave Ramsey’s teachings on debt consolidation loans offer a refreshing perspective on financial management. By focusing on behavior change, discipline, and long-term solutions, Ramsey empowers individuals to break free from the cycle of debt. While debt consolidation loans may seem like a quick fix